Cashback credit cards remain a smart tool for turning everyday spending into tangible savings.

With Belgium’s evolving financial landscape now offering cards that combine global usability, competitive rebate rates, and user-friendly terms, consumers can unlock meaningful returns on routine purchases.

This article explores the top cashback card options available, outlines their key features, and provides actionable tips for getting the most value from every euro you spend.

Why a Cashback Card Still Matters Today

A cashback credit card turns ordinary spending into direct money back, freeing extra cash for future goals or emergency buffers.

Belgium’s market now includes products that pay competitive rates, work worldwide, and remove many old-style barriers, so you can extract tangible value without complicated reward hoops.

Identify Your Spending Profile First

A quick self-audit clarifies which card structure fits best and prevents mismatched expectations.

Spending varies widely, yet four pillars shape the ideal cashback card choice:

- Everyday Purchases Dominate

Grocery runs, streaming subscriptions, and public transport fares will quickly rack up rewards when the card pays a flat rate on broad categories. - Seasonal Big-Ticket Outlays

Garden upgrades or electronics splurges deserve a card that raises its cashback multiplier during promotional windows or offers an unlimited spending ceiling. - Frequent Worldwide Travel

Cards waiving foreign-purchase fees and offering multilingual support keep costs predictable across borders, whether the transaction happens in Brussels or beyond. - Privacy-Driven Usage

If anonymity ranks high, select a provider that issues tokenized numbers and asks only for a passport, email, and phone during Know-Your-Customer checks.

Key Features That Differentiate Belgian Cashback Cards

Understanding core mechanics streamlines comparison and prevents surprises in the first statement cycle.

Anonymous Transactions

Providers such as FXP Credit Card adopt virtual card numbers and minimal data collection. This structure shields your identity during online purchases, a plus for privacy-minded users.

Unlimited Spending Potential

Several fintech cards drop preset limits once income verification clears, allowing large purchases without piecemeal pre-approvals. This is valuable when buying furniture or paying annual tuition in one go.

Simple KYC Workflow

Traditional banks often request employment certificates and utility bills. Modern rivals need only a valid passport, email, and mobile number, reducing onboarding to minutes rather than days.

Transparent Annual Fees

Many Belgian issuers now publish a single flat yearly charge, sometimes zero, rather than layered maintenance fees. A clear fee table helps determine whether the cashback easily cancels out the cost.

Competitive Purchase APR

Interest rates still vary; cards marketed at younger audiences can reach 18%–20 % variable, while premium tiers sit closer to 12 %. Plan to clear balances monthly to preserve every euro earned.

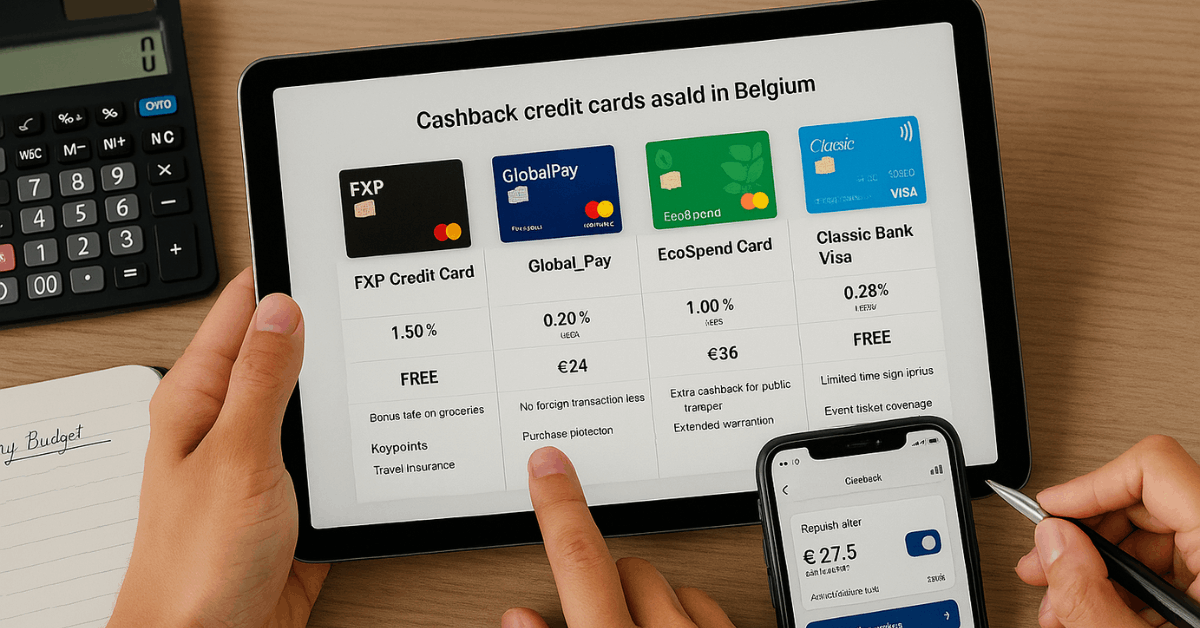

Top Cashback Credit Cards Available in Belgium

The lineup below highlights widely issued products that balance reward rates, worldwide acceptance, and straightforward terms.

- FXP Credit Card – “Cashback Sans Limite”

- 1.25 % flat cashback on all eligible spend, worldwide.

- Zero annual fee for the first year, then €48.

- Foreign-transaction fee: 0 %.

- The application requires a passport, email, and a Belgian phone number only.

- Spoken language support: English, French, Dutch.

- GlobalPay Unlimited Card – “Retour Argent Illimité”

- 2 % cashback on supermarket and fuel, 0.5 % elsewhere.

- Unlimited spending threshold once verified income exceeds €1 800 monthly.

- Annual fee: €35, waived when yearly spend tops €9 000.

- EcoSpend World – “Carte Monde Éco-Cashback”

- 1 % base rate, plus 0.5 % bonus when transactions are logged at certified eco-merchants.

- Optional digital-only mode for anonymous online purchases.

- Payback credited monthly directly onto the statement.

- Classic Bank Cashback Visa – “Visa Remboursement Classique”

- Tiered structure: 0.5 % below €6 000 yearly spend, 1 % above.

- Traditional branch network for in-person service.

- Purchase APR: 13.99 % variable.

How Cashback Mechanics Actually Pay You

Knowing settlement timelines helps match expected earnings with real cash arrivals.

- Spend Clears the Network

Merchant submits the charge via Visa, Mastercard, or private rails. - Issuer Receives Interchange Fee

Part of this fee subsidizes your cashback. - Cashback Tallied

Each posting date pushes the transaction into that month’s rewards ledger. - Payout Issued

Most Belgian cards credit statements monthly; some send SEPA transfers to your current account every quarter.

Strategies to Maximize Returns

A systematic approach ensures cashback still beats alternative reward formats such as airline miles.

- Consolidate Purchases

Funnel routine bills, utilities, telecom, insurance, onto one high-rate card to keep the reward pool concentrated. - Hit Annual Fee Waivers

Cards like GlobalPay remove yearly costs once predefined spending thresholds are met. Scheduling big purchases early helps clear that bar sooner. - Automate Full Repayment

Setting automatic SEPA direct debit for the entire balance sidesteps interest, protecting net cashback earned. - Monitor Promotional Boosts

Many issuers run seasonal multipliers on categories such as home improvement. Take advantage when planning significant renovations.

Common Pitfalls and How to Avoid Them

Protect gains by steering clear of hidden costs and policy traps.

- Ignoring Exclusion Lists

Gambling transactions, cryptocurrency purchases, and ATM withdrawals rarely offer cash back. Read the issuer's brochure carefully. - Missing Introductory Deadlines

Some cards advertise elevated cash returns for the first three months only. Track opening dates to concentrate spending during that window. - Carrying a Balance

Interest at 18% quickly outweighs a 1% rebate. Full repayment remains the simplest safeguard. - Overlooking Foreign-Transaction Fees

A card may boast 2% cashback yet still levy 2% currency fees outside the eurozone, nullifying the benefits. Check the schedule of charges before international travel.

Debit-Card Alternatives Worth Consideration

Certain fintech debit products mimic cashback features while reducing the risk of revolving debt.

- RevoluPay Metal – 0.1 % Cashback Worldwide

Lower rate but instant payout into the wallet. - N26 Smart – Partner Retailer Kickbacks

Fixed euro amounts returned on qualifying purchases rather than percentages. - Bunq Easy Money – 2 % Green Cashback on Public Transport

Appeals to eco-conscious commuters.

Quick FAQ

You might ask these questions along the way:

- What matters most when selecting a Belgian cashback card?

Prioritize spending habits, fee tolerance, credit approval odds, and global usability. - Which cards suit frequent travelers?

Options such as FXP Credit Card or classic airline cobrands waive foreign-purchase fees and include baggage delay coverage. - How is cashback delivered?

Most issuers credit the statement monthly; some transfer to a linked current account on request.

Conclusion

Selecting the best cashback credit card in Belgium demands aligning personal spending patterns with card features such as anonymous transactions, unlimited limits, and transparent fees.

Compare at least three issuers, read every fee schedule, and automate full balance payments. Equipped with these steps, you can turn everyday outlays, across Belgium and worldwide, into reliable, hassle-free income streams.