Instead of issuing loans itself, Bright Money pairs you with partner lenders. A soft check allows you to compare estimated rates and terms up to $100,000, without it affecting your credit score.

The selected lender handles the final approval and funding. Bright also provides tools to help you manage your balance and build credit.

What Bright Money Is and What It Isn’t

Bright Money operates as a matching service rather than a direct personal-loan lender.

Partner lenders provide offers, and prequalification can check eligibility without affecting your credit score, letting you compare potential rates and terms up to an advertised $100,000 limit.

Final approval, funding, and exact terms come from the partner that underwrites the loan.

How Matching Works

Bright collects basic details, runs a soft eligibility check, and shows partner offers if you qualify. Subsequent application with a chosen lender may involve a hard inquiry, standard identity verification, and full underwriting before funds are released.

Direct Products Beyond Loans

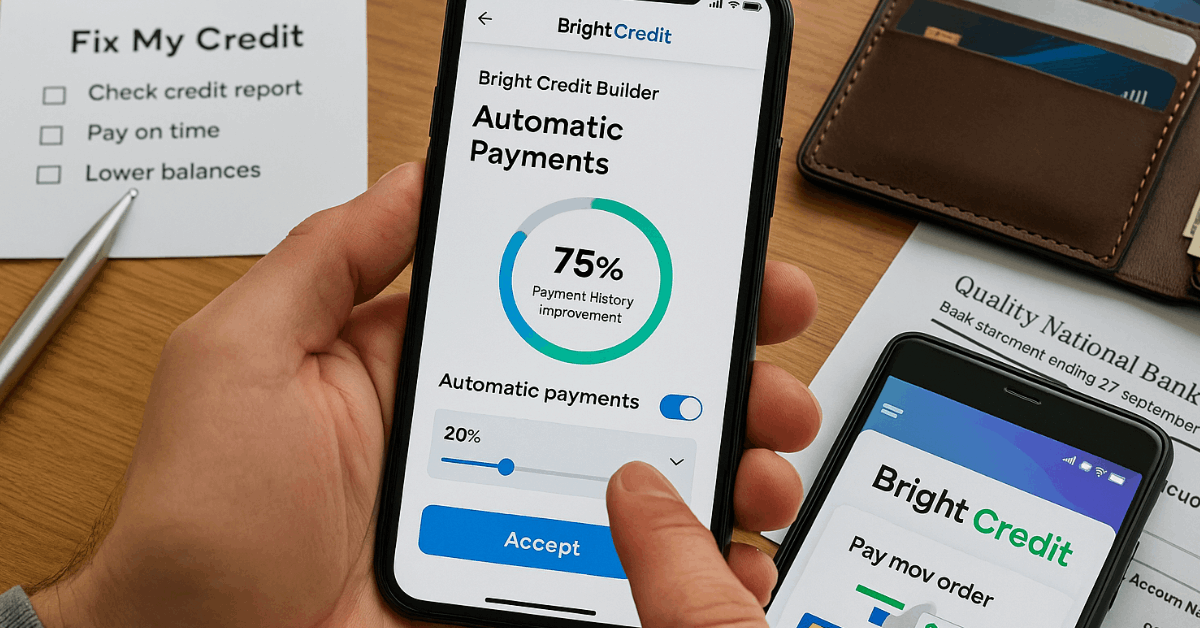

Bright also markets in-house credit tools. Offerings include a balance-transfer style line of credit aimed at paying down card debt and a credit-builder program that automates small on-time payments to help improve credit factors.

How Bright’s Personal-Loan Matching Works

Need a quick comparison without risking a score drop during the initial check? The flow below shows what to expect before applying with any specific lender.

- Choose an amount: Select a target up to $100,000 based on need and repayment capacity, not just maximum availability.

- Prequalify: Provide basic personal and financial data for a soft check that does not impact your score.

- Compare offers: Review APRs, terms, fees, and monthly payments across partner options; confirm the one that fits your budget.

- Complete application: Apply with the chosen lender; after approval, funds are deposited to your account by the lender.

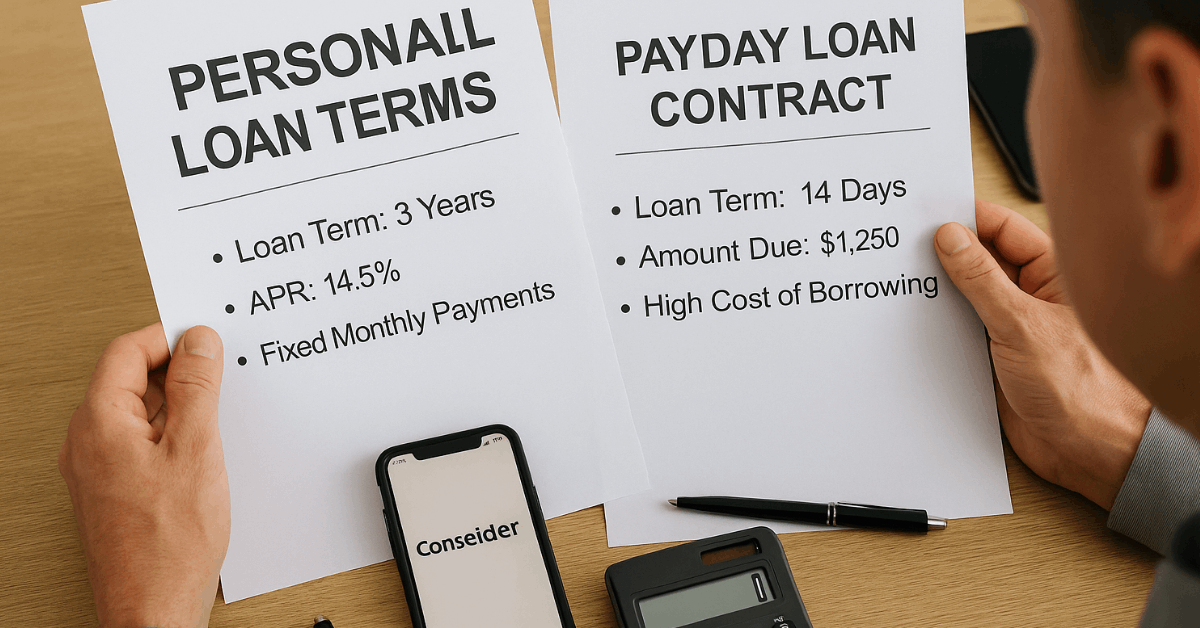

Personal Loans vs Payday Loans: Key Differences

Sticker shock and short timelines push many borrowers toward fast cash, yet costs and risks differ sharply. Use the side-by-side view to anchor the decision.

| Feature | Personal Loan | Payday Loan |

| Typical APR | About single- to mid-30s, based on credit and income | Often triple-digit effective APR |

| Loan Amount | Usually hundreds to $100,000 | Usually $100 to a few hundred |

| Repayment Term | Fixed monthly installments over months or years | Due in full by next payday |

| Credit Check | Full underwriting; builds credit with on-time payments | Minimal checks; limited credit building |

| Risk Profile | Structured payoff; lower risk of spirals if budgeted | High rollover risk and fee stacking |

When Each Option Fits

Personal loan, stable income, a clear payoff plan, and a need for a larger sum favor an installment loan. Debt consolidation, medical costs, and home improvements align well, because predictable payments and potentially lower APRs can reduce total interest when compared with revolving balances.

Payday loan, genuine emergencies, very small amounts, and no available alternatives sometimes leave a payday advance as a last resort.

Strict repayment on the next paycheck and very high costs require a realistic payoff plan and immediate exit strategies to avoid rollovers.

Eligibility, Rates, and Costs of Personal Loans

Lenders price loans using credit score, debt-to-income ratio, verified income, and overall profile. Secured loans pledge collateral such as a vehicle or home, often trading lower rates for asset risk.

Unsecured personal loans skip collateral yet typically require stronger credit and may carry higher APRs.

Total cost depends on APR, fees like origination or late charges, and term length; shorter terms increase monthly payments while cutting lifetime interest. Payment history and utilization changes report to credit bureaus, so missed payments hurt scores and may trigger fees.

How to Apply for a Personal Loan

Unexpected costs demand speed, but smart sequencing prevents expensive mistakes. Follow these essentials before committing.

- Check credit and DTI: Pull reports, dispute errors, and calculate debt-to-income to gauge realistic approval odds and rate tiers.

- Compare lenders: Weigh banks and credit unions for potential lower rates against online lenders that emphasize speed and flexible credit bands.

- Prepare documents: Gather ID, income proofs, bank statements, and debt lists to avoid delays and re-requests.

- Evaluate full APR and fees: Prioritize total cost, not teaser rates; understand prepayment, late, and origination fees.

- Automate payments and monitor: Enable autopay, track due dates, and adjust budget early if a payment risk appears.

Alternatives If a Personal Loan Doesn’t Fit

Consider these alternatives if you can't apply for this loan:

Balance Transfer or Personal Line of Credit

Lower-APR balance transfer offers or a personal line of credit can manage revolving balances while preserving flexibility, although transfer fees and variable rates require careful math and discipline.

Home Equity Options

Home equity loans or HELOCs may deliver lower rates when substantial equity exists, while placing your home at risk if repayment falters.

Credit-Builder Loan or Secured Card

Structured programs that report on-time payments help strengthen thin or damaged files, improving access to better credit later.

Community and Hardship Support

Nonprofits, employer hardship funds, medical bill assistance, and negotiated payment plans often reduce immediate pressure without high-cost debt.

Bright Money Products to Consider Instead

Bright Balance Transfer provides a dedicated line intended to pay down high-APR card balances, reportedly up to $10,000, with APRs starting near 9.95% based on eligibility. Funds move to selected cards, and Bright then automates repayments toward that line, aiming to reduce interest expenses and simplify payoff.

Bright Credit Builder sets up an interest-free, secured line that makes automated small payments to report positive activity and lower utilization on linked cards. Improved payment history and utilization can support gradual score gains, which may unlock cheaper future credit.

Bright Plan uses its MoneyScience approach to schedule and optimize payments across accounts. Budget-aware automation can reduce missed-payment risk and keep payoff momentum consistent over time.

FAQs: Quick Answers

Fast decisions depend on clear expectations; the points below address common concerns raised during loan shopping.

- Are payday loans ever reasonable for emergencies? Only as a last resort when no other credit is available and repayment on the next payday is certain, due to very high costs and rollover risks.

- Can a personal loan work with bad credit? Some lenders approve lower credit tiers at higher APRs; adding a co-signer or collateral and improving reports beforehand can help.

- What happens after a payday-loan default? Additional fees, collections, and credit damage typically follow; communicating early with the lender and seeking assistance programs can limit harm.

- How do you break a payday-debt cycle? Build a realistic budget, negotiate payment plans, increase income where possible, and work with nonprofit credit counselors to restructure obligations.

- Do “no credit check” loans make sense? Extremely high effective costs and fee structures make such products risky; safer alternatives should be exhausted first.

Conclusion

Bright’s marketplace approach can surface multiple partner offers quickly through a soft eligibility check, aiding rate and term comparison without an initial score hit.

Borrowers who need structured funds for legitimate expenses stand to benefit most, provided total costs and repayment capacity are verified.

Those facing very short-term, small-dollar gaps should avoid payday loans whenever possible and consider safer alternatives or Bright’s debt-paydown tools.