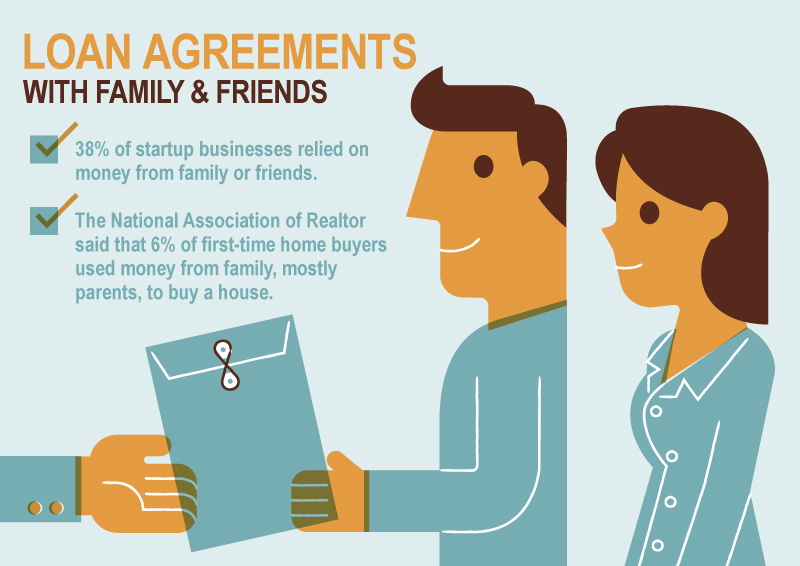

Money is an extremely sensitive matter. It can either bring people together or completely destroy their relationship. According to the Federal Reserve Board, loans between family members and friends usually amounts to around $89 billion each year in the US.

Most of the reasons for borrowing this money range from purchasing a home to starting a business. One of the biggest problems that can occur with the family lending process is taxes and personal consequences, especially when lending money to purchases a home. If this process is not documented properly, or not documented at all, then problems will arise.

For this reason, we tell you about the National Family Mortgage. This company helps you set up your own mortgage for your relatives. They help the lenders make the loans feel good and prevent any potential tax problems. They also protect the lenders and ensure they get repaid.

How Does It Work?

National Family Mortgage helps the borrowers to also fund their dreams of homeownership and stay on track with all mortgage payments.

The lenders also generate solid returns from their investments at rates similar to what they would earn from a money market or bonds. When you know your money is secured through a registered mortgage, then you can be free to lend, even at low-interest rates.

Most families also choose to use the National Family Mortgage for the simple purpose of preventing the scrutiny from the IRS on federal gift tax returns. Others use them to protect the wealth of their family in case the borrower dies or gets divorced.

They provide a legal structure with tax benefits and unmatched flexibility that is a win-win for both the borrowers and the lenders.

Refinancing A Mortgage

Lending money to loved ones through the National Family Mortgage can get you some solid returns similar to the returns you would receive from CDs, bonds, and other savings accounts.

If a family member wishes to refinance their loan, the lenders can claim the popular home interest deduction using the old IRS cap. However, it is limited to less than $500k for single borrowers and up to $1 million for married couples.

Renovating A Home

Borrowers can deduct their mortgage interest on debt, which includes interest charged on the loan and what is used to pay the actual costs of any home improvements. However, this is only if their loans are secured using their homes.

Under the tax code of the IRS, any substantial home improvements that add value to your home and that prolongs its life are considered a substantial home improvement. The interest deduction, however, is limited to at least $375k for individuals and $750k for married couples.

The Reverse Mortgage

The National Family Mortgage has a product they dubbed Caregiver Mortgage. This is a family-funded reverse mortgage product that offers homeowners a line of credit. It features most of the benefits you would get from a bank’s reverse mortgage product, although their product doesn’t have the restrictions and high costs.

As a borrower, you can generate a tax-free revenue stream from your family members and live comfortably from it. You can also enjoy retirement when you know that you are building your family’s future.

As a lender, you can empower your loved ones with a smart solution that can provide predictable financial support that is completely flexible and will be repaid.

Borrowing Home Equity

An intra-family equity home loan is a great solution when consolidating and refinancing credit card and student loan debts. If you are self-employed, this loan product is a great alternative to institutional business loans.

This type of loan product is perfect for your family members who wish to use it for non-real estate purposes such as paying for school or the other purposes noted above. However, please note that the IRS eliminated this deduction in 2018.

Conclusion

While lending to family members seems like the most stress-free option, it is important to ensure that everything is in order in terms of the taxes and other requirements. Thankfully, National Family Mortgage can help you with this!